[PDF] The Value At Risk VAR In The Banking System Ebook

Capital Adequacy Basel 2 Financial Institutions

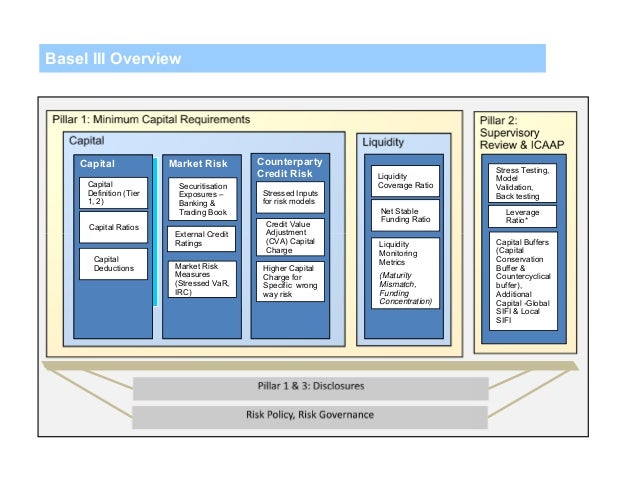

James Okarimia Basel Iii Presentation

Settlement risk - Wikipedia Settlement risk is the risk that a counterparty (or intermediary agent) fails to deliver a security or its value in cash as per agreement when the security was traded after the other counterparty or counterparties have already delivered security or cash value as per the trade agreement. The term covers factors incidental to the settlement process which may suspend or prevent a trade from ... Readings Financial Risk Management (FRM) GARP Chapter 1 (p 3-24) Michel Crouhy, Dan Galai, and Robert Mark, The Essentials of Risk Management, 2nd Edition (New York: McGraw-Hill, 2014). Value at risk - Wikipedia Value at risk (VaR) is a measure of the risk of loss for investments.It estimates how much a set of investments might lose (with a given probability), given normal market conditions, in a set time period such as a day.

Eigencat Digital Investment Solutions

Notes From Rational Support Blog

British Airways Wikis The Full Wiki

0 Response to "The Value At Risk VAR In The Banking System"

Post a Comment